An excellent article from one of our members

Due to the markets falling and the impact of COVID-19, there has been major impacts on the balance of KiwiSaver funds and Investment funds.

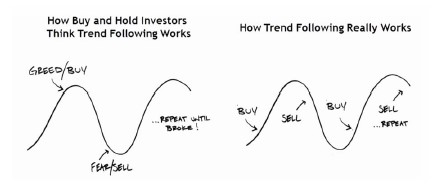

Make no mistake, this market correction is not normal, so it is OK to feel strange about any investment you may have. The last time markets fell this far and fast was 2008 during the Global Financial Crisis, and before that in 2000 with the Tech Bubble burst, so this is the 3rd time in 20 years. Although we were able to foresee this fall to a degree, we hadn’t expected it to be this violent. What history tells us about those falls, is that the market has come up substantially since 2008 and has been accelerating in recent years so it needed to let off some steam.

There is no point changing investment strategy when the market has fallen, you must do this before a fall!

What should we expect next?

All markets follow a rhythm. Major downturns in markets correlate with economic recessions, which are often determined after the event as GDP growth is slow to report – usually many months after the event.

Economic fundamentals and quantitative analysis both suggest we are entering a bear market (negative) phase of the business cycle. As such, the current environment is unlikely to be a quick drop followed by a quick recovery, with volatility likely to last for some time. These market conditions usually experience big falls punctuated by sharp rallies. Falling markets provide fund managers with a massive opportunity to buy companies at cheaper prices, which should align with your elected risk profile.

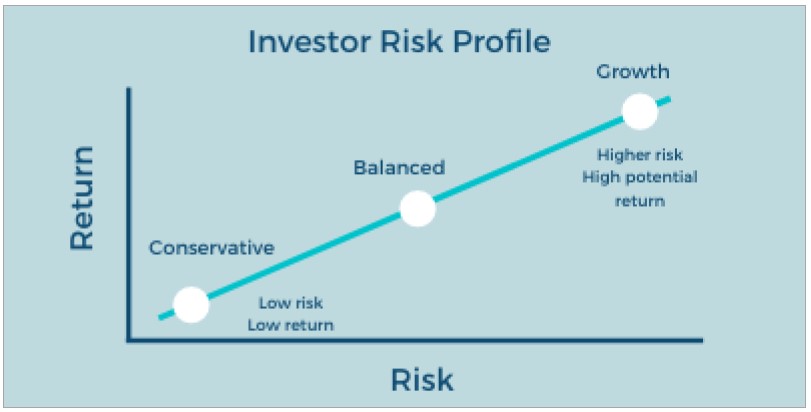

Risk Profile 101 – What are your goals?

Conservative – You don’t like volatility and don’t mind getting lower returns. Focusing on possible losses is important to you. This will be someone nearing retirement or looking to buy their first home. A good example is the first home buyers on TV recently, concerned about their investment value dropping, when ideally if they had good financial advice, they should have been in a fund that wouldn’t sustain such dramatic falls.

Balanced – You want middle of the road returns, willing to accept some moderate fluctuations to get average long term returns. You will be in your 50’s and thinking about building up a nest egg to protect at age 65.

Growth – You are investing for the long term and don’t mind volatility. You are focusing on gains and don’t mind losses to get above market returns Your typical growth fund has a mandate to be invested in 90% shares, therefore if the market goes up – all good. If it goes down, then it really goes down.

Everyone is saying it and it is true

It is too late to lower your risk profile during a correction, so you need to stay the course. Most Balanced Growth or Growth funds increased by over 15% last year, and now the market has pulled back to where it was in the middle of 2017. When it increases from here, it will be making up this ground. It is haunting losing money, but you must be pragmatic that time in the market is the best solution.

Tim Fairbrother

Authorised Financial Adviser

The information is of a general nature and is not intended as personalised financial advice. We recommend speaking to your adviser before purchasing, changing or disposing of any financial products.